Should You Switch to EveryDollar? An Honest Review

Budgeting apps are trendy and all, but I’ve got my equally cool budget (and expense tracking) spreadsheet over here, thank you very much.

(I’d like to say I’m not married to my systems, but that’s not completely true!)

Still, I’m not against trying new things. I really did want to try EveryDollar and see if it solidified my time-tested budgeting process…

Or if it would maybe, just maybe (gasp!) inspire me to change things up!

What is EveryDollar?

EveryDollar is a simple budgeting app (also available on desktop!) that supports the zero-based budgeting method.

Wait, what’s that? Basically, with this method, you plan ahead and “spend” your paycheck by divvying it up among all your monthly bills and expenses. The main goal: to have $0.00 left over, so there’s no money hanging around “unbudgeted,” or without an assigned category.

Then at the end of the month, if you have money left over, you “zero” out and roll that into your savings. (For more on this method, here’s this article by Dave himself.)

So, what did I think?

I make the best decisions when I organize my thoughts about new processes into list of pros and cons (something my dad taught me!). So without further ado, here’s my opinion on the EveryDollar app after a month of using it myself.

Pro #1: Easy-to-Use App

With my budget spreadsheet, I have to pull up Google Sheets manually and enter in all the transactions on my laptop. With EveryDollar, adding a transaction is incredibly simple.

All you have to do is:

- Enter the amount

- Choose the date when you spent that amount

- Type in your merchant (store/restaurant name, etc.)

- Choose from your list of budget categories

- Split the transaction if you need to (i.e. from a Target shopping trip where you spent money in the clothes, pet food, and groceries categories)

This entire process takes a matter of 15 seconds tops!

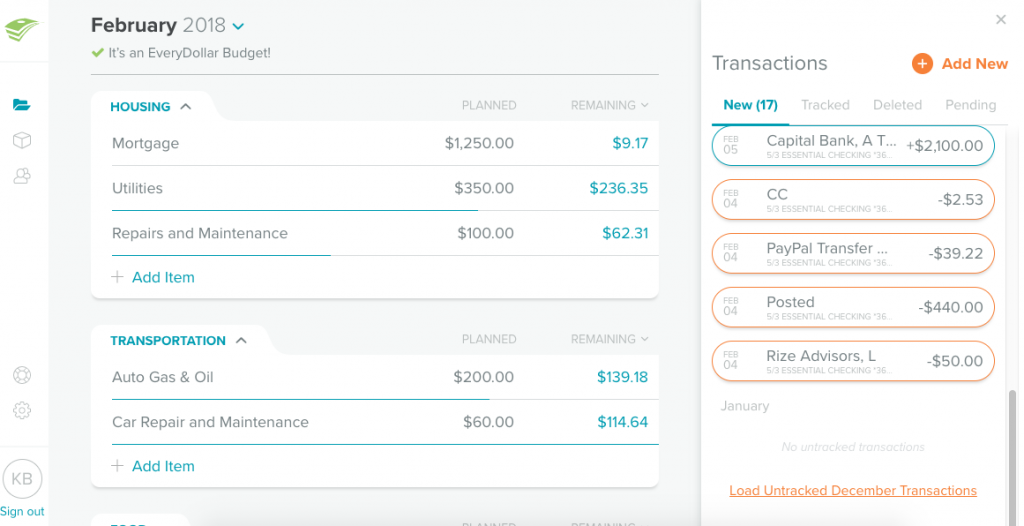

![]()

EveryDollar is also accessible from your desktop, but if you use the FREE version, it’s just as easy to do everything on the app. Plus, the app syncs between multiple users in your household which means everyone knows exactly what’s being spent and how much is left.

Pro #2: Detailed Categories

Keeping our categories fairly broad is a great way to see everything at a glance on my spreadsheet without scrolling back and forth, but it can also lead to overspending and not knowing how much I actually spend in certain areas.

For instance, Joseph and I have a column labeled “Variable Expenses” which covers all groceries, toiletries, paper products, and pet care. We also tend to go negative in that “account” because we are not adequately budgeting for each individual category included!

It’s very easy in EveryDollar to create as many main and sub-categories as you need and they are super easy to scroll through to see what you plan to spend, what you’ve already spent, and what you have remaining in that budget category.

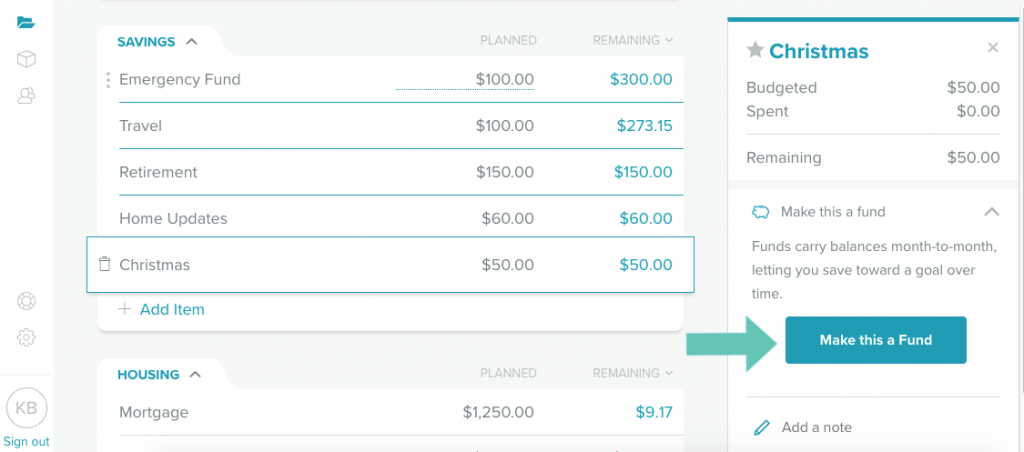

Pro #3: The ability to create “funds”

For expense categories that don’t get paid/used every month and that you want to build up (examples would be car insurance, car repairs, house repairs, Christmas gifts, etc), you can create a FUND.

By establishing a category as a fund, what you save each month becomes a balance that rolls over from month to month (as opposed to zeroing out that amount at the end of the month). This allows your fund to grow until you need it down the road.

The only downside to this feature is if you spend more than you budgeted to spend in a fund for the month, the account turns red like you’ve gone negative, when you actually haven’t because you’ve been saving for months already.

Example: Our Medical Fund had $382.58 in it at the beginning of February. We budget $120 dollars for it every month. Even though in February we spent $344.28 and still have $158.30 remaining, EveryDollar says we spent too much.

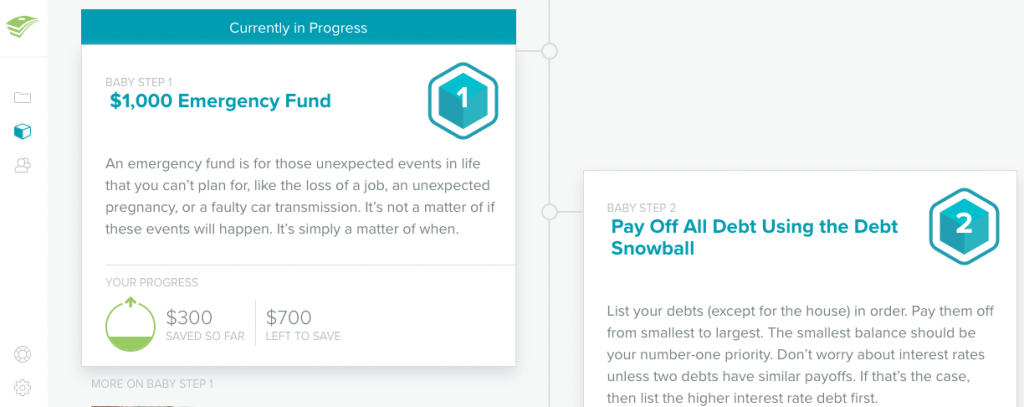

Pro #4: Integrates with the Dave Ramsey Baby Steps

If you’re familiar with Dave Ramsey’s teaching method, then you already know his seven baby steps. From creating an emergency fund to paying off your home, EveryDollar integrates your everyday transactions into whatever baby step you’re tackling right now.

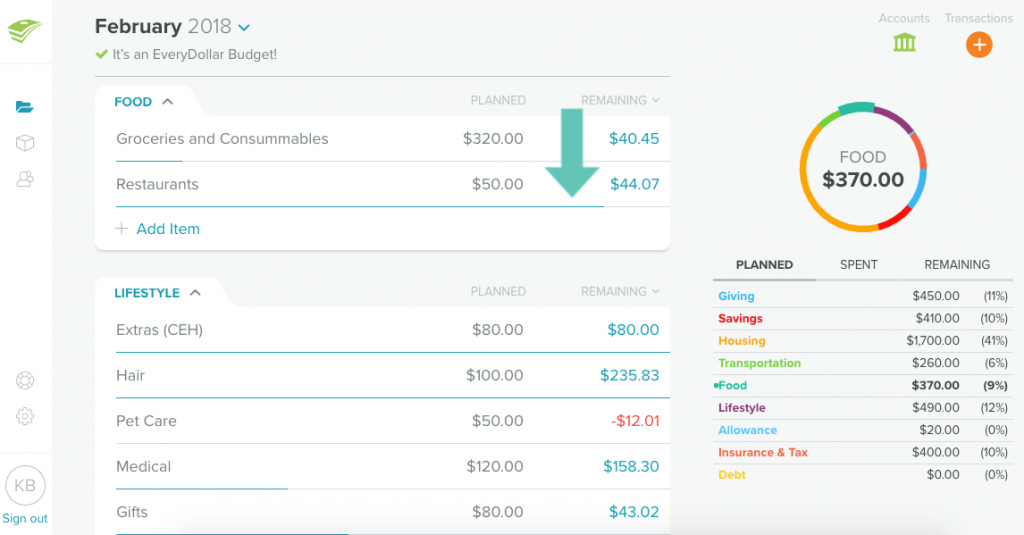

Con #1: Focuses only on a MONTHLY budget

EveryDollar adds all the income you receive in a month together to be budgeted out on a monthly basis, rather than a biweekly basis. So instead of budgeting per paycheck like I normally do (i.e. a paycheck comes in and then I divide it among my budget categories), you budget your month BEFORE you receive any paychecks.

My concern with this method was that I would spend money faster in a category than I actually should and have barely any money left by the end!

What if I went on a grocery shopping spree and spent $300 on groceries because EveryDollar says I can? I might have a full pantry for the full month but no budgeted money with which to buy fresh produce that fourth week.

With my per-paycheck method, it’s easier to spread out that money over two weeks than it is two paychecks over four weeks.

EveryDollar does display a blue line underneath each category to show you what percentage you’ve spent (half, less than half, etc), but I would prefer an alert sent to my phone, kind of like the one my data plan sends… “at this rate, you’ll run out of money by X.”

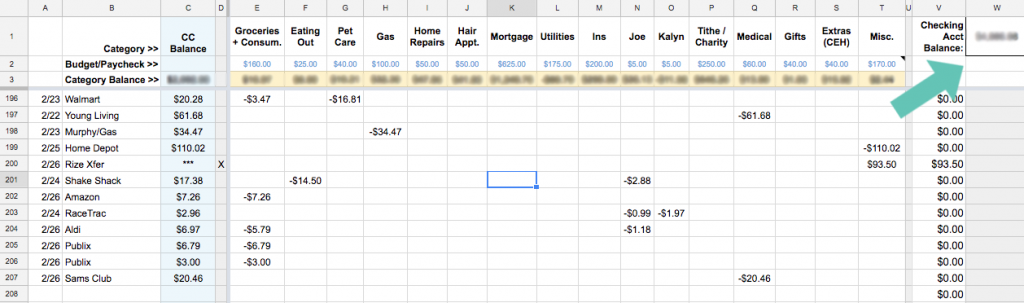

Con #2: Doesn’t Balance with Your Checking Account

In addition to budgeting per paycheck rather than per month, I also make sure the sum of ALL my budget categories equal my total checking account balance. Basically, every penny in my checking account needs to be assigned somewhere, even if it ends up in the Misc. category!

So in the screenshot below, the amount left over or what I call the “category balance” should equal the total in my checking account. If it doesn’t, then I know I’ve missed a transaction somewhere and can investigate where that money went.

As far as I know, EveryDollar can’t do this.

But YNAB can! I’ve now completely switched my finances over to YNAB. Here’s why.

The Everydollar app shows your budgeted amounts for each category as well as your bank account balances (if you upgrade to the annual plan), but it doesn’t make sure both of those features equal each other. This means you probably have some money hanging out in your checking account that isn’t assigned anywhere.

Of course, this may not bother you and in that case, this probably isn’t a con at all! (As long as you always have an Emergency Fund to cover those months where a big bill leads you to spend more than you make!)

Con #3: Hefty Annual Fee

If you upgrade to EveryDollar Plus, you’ll pay $99 a year for priority support and the ability to connect to your bank and credit card accounts which will automatically import all transactions. From there, you can drag and drop each transaction into the specific category or split it into two different categories.

I feel like that’s a pretty hefty price point for convenience. It doesn’t take much time at all to manually enter transactions or spend five minutes a day to check your accounts and make sure you’ve entered in everything.

However, if you haven’t done Financial Peace University yet (Dave Ramsey’s signature program), you can get a one-year membership to EveryDollar Plus as part of their package offer.

In Summary

Even though (for me) there are more pros than cons to using EveryDollar, the significance of the cons far outweigh the pros. In other words, I’ll be sticking with my Excel spreadsheet!

But that might not be the case for you. Here’s how to know if EveryDollar could be your budgeting match made in heaven.

If you…

- Don’t feel the need to micromanage your money, but still want a budget

- Like the ease of adding transactions on your phone and having it sync automatically with your spouse’s phone

- Love Dave Ramsey and want to keep track of your baby steps and budget in the same tool

- Are already familiar with zero-based budgeting and budgeting on a monthly basis

Then EveryDollar will quickly become your favorite budgeting app!

But if not, you can always check out my budgeting series where I show you how to set up an Excel spreadsheet like mine, or look into another software like Mint or You Need a Budget (YNAB).

Need more information before you decide?

- My friend Rachelle’s review of EveryDollar comes from someone who used the app to save up for her wedding–and her first home!

- My friend Rosemarie also loves EveryDollar!

- Here is a thorough EveryDollar set-up video tutorial by Freedom in a Budget.

- This EveryDollar Q&A with Rachel Cruze (Dave Ramsey’s daughter) tackles users’ most frequently asked questions, including the split-transaction feature and budgeting on irregular income.

- And of course, be sure to check out the official EveryDollar.com website.

Let’s chat about budgeting tools!

Have you tried EveryDollar or some other budgeting app?

Disclosure: Some of the links in the post above are affiliate links. This means if you click on the link and purchase the item, I will receive an affiliate commission. Regardless, I only recommend products or services I use personally and believe will add value to my readers. Read my full disclosure policy here.

We just budget for the whole month, so it works for us. Jane (above) mentioned breaking categories down my the week. We did that for awhile, but decided, for us, that weekly breakdowns were more confusing. Although I have never done it, maybe budgeting by the week can be done by just adding weekly (bi-weekly, etc.) income and only the bill amounts that will be paid with that check. I would still list all outgoing categories, but only add planned amounts when that check hits. Does that make sense? I also add a checking account cushion each month so that we always keep that amount in the account after all bills and expenses are paid. It’s easy to use, like you said, and works for us for now. Although, the reports YNAB generates sound very appealing!

Makes total sense! Buffers are always good as well and you can do that in YNAB as well just by creating an extra category and calling it “buffer.” I always think at the beginning of the month that I won’t need that…but somehow we always need some buffer.

This is a great review!

In case if someone would decide to go with the app and still has concerns about Con #1 i have an idea how it can be fixed:

Create a Category and break it down to Week 1, Week 2 etc. Set a budget for each week and that way you won’t spend the entire Grocery budget in the first week…

Just a thought. Hope it helps others.

Thank you for all the info!

Thanks for the tip, Jane. 🙂

This was a really good overview of Every Dollar, Kalyn! Thank you so much for the ‘need more information’ section too, I appreciate the video link!

You’re welcome, Melissa.

It’s so impossible to cover everything in on review I wanted readers to be easily able to find more information and different perspectives.